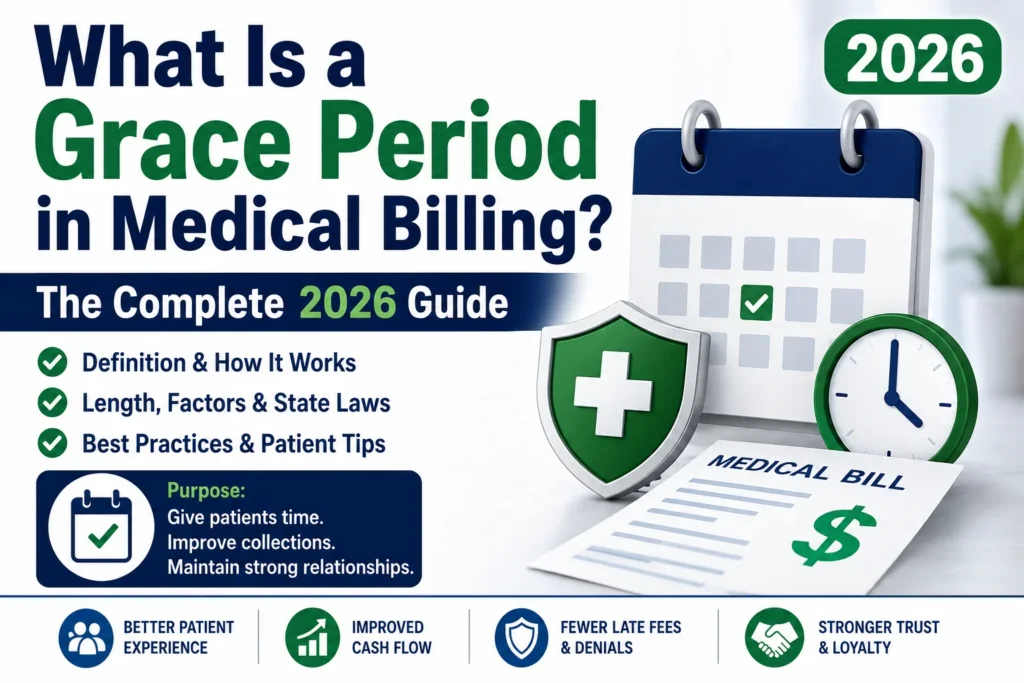

What Is a Grace Period in Medical Billing? The Complete 2026 Guide

What Is a Grace Period in Medical Billing? The Complete 2026 Guide Here is a scenario every billing team has lived through: a claim goes out clean, sits for weeks with no denial and no payment, and when someone finally calls the payer, the answer is “the patient is in their grace period.” Nothing was […]

Disability vs Mental Health | The Difference That Matters 2026

Disability vs Mental Health | The Difference That Every Practice Should Understand 2026 Here is the confusion that costs patients their benefits and practices hours of rework: a mental health diagnosis and a disability are not the same thing. When people search “disability vs mental health,” they are usually trying to untangle exactly that — […]

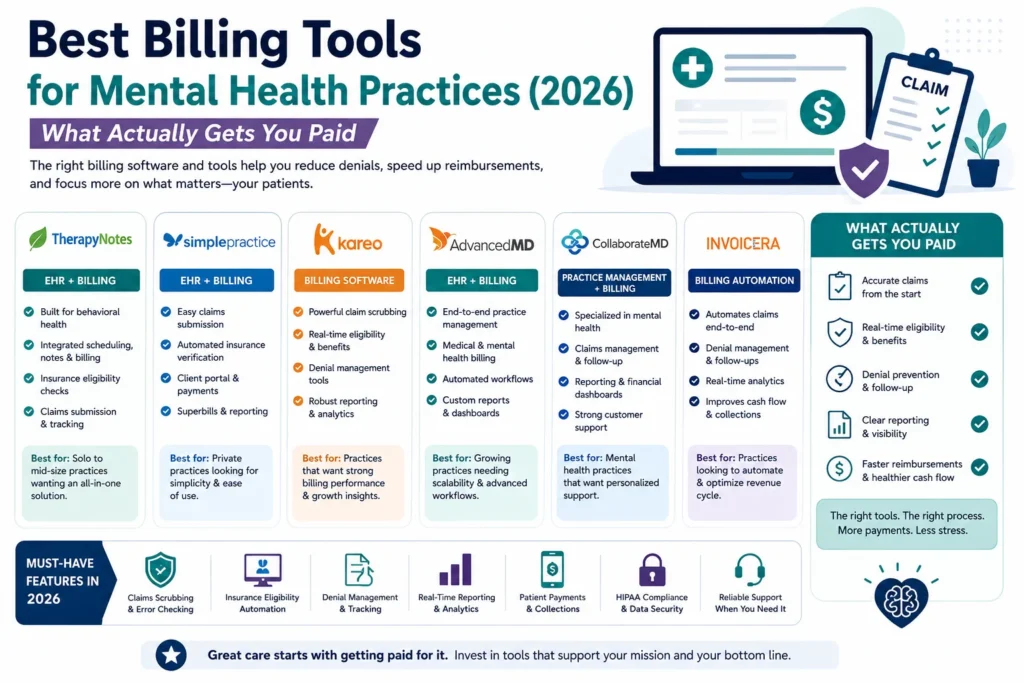

Best Billing Tools for Mental Health Practices 2026 Guide

Best Billing Tools for Mental Health Practices (2026) — What Actually Gets You Paid Choosing the best billing tools for mental health practices usually comes down to a question people forget to ask: not “which software has the nicest interface,” but “which one actually gets my claims paid on the first pass?” The most expensive […]

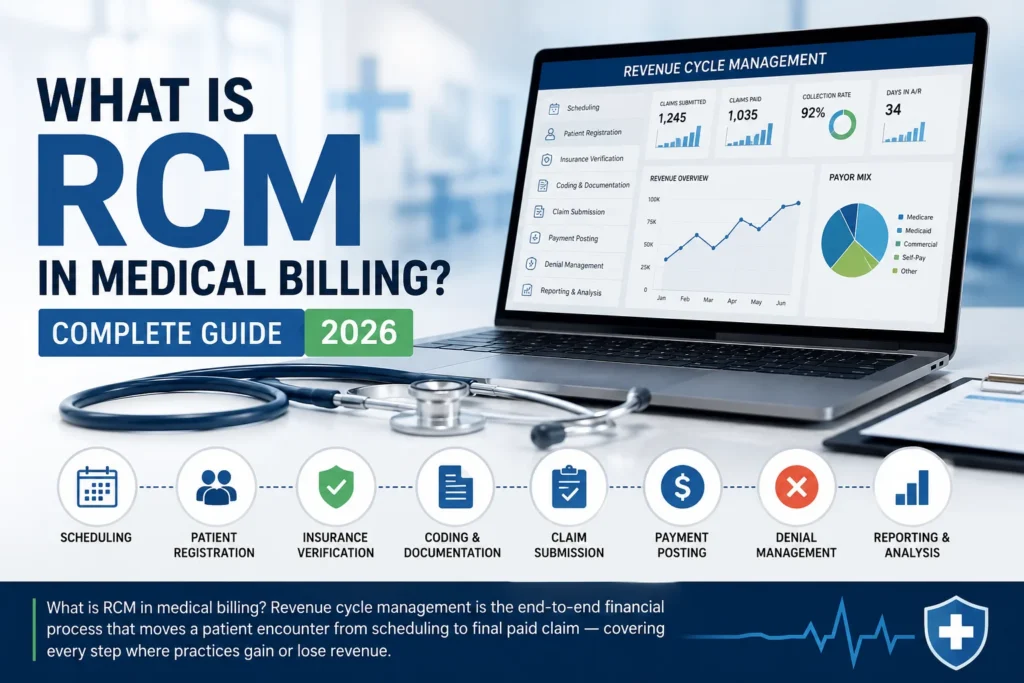

What Is RCM in Medical Billing? Complete 2026 Guide

What Is RCM in Medical Billing? Complete 2026 Guide for Healthcare Practices If you have ever asked yourself why your practice seems to be busy all the time but the bank account does not reflect it — RCM is usually the answer. RCM stands for Revenue Cycle Management. In medical billing, it refers to the […]

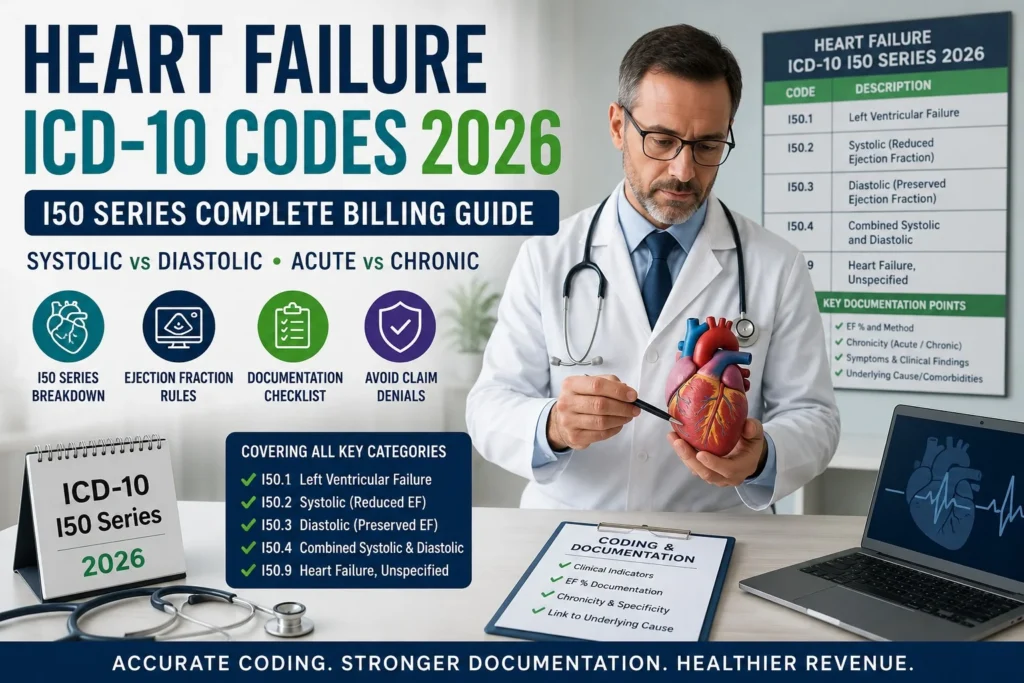

Heart Failure ICD-10 Codes 2026 — Complete I50 Series Billing Guide

Heart Failure ICD-10 Codes 2026 — Complete I50 Series Billing Guide Of all the coding decisions in cardiology, heart failure is where the most expensive mistakes happen. Not because the codes are hard to find. Because coders default to I50.9 — unspecified heart failure — when the clinical documentation actually supports a far more specific […]

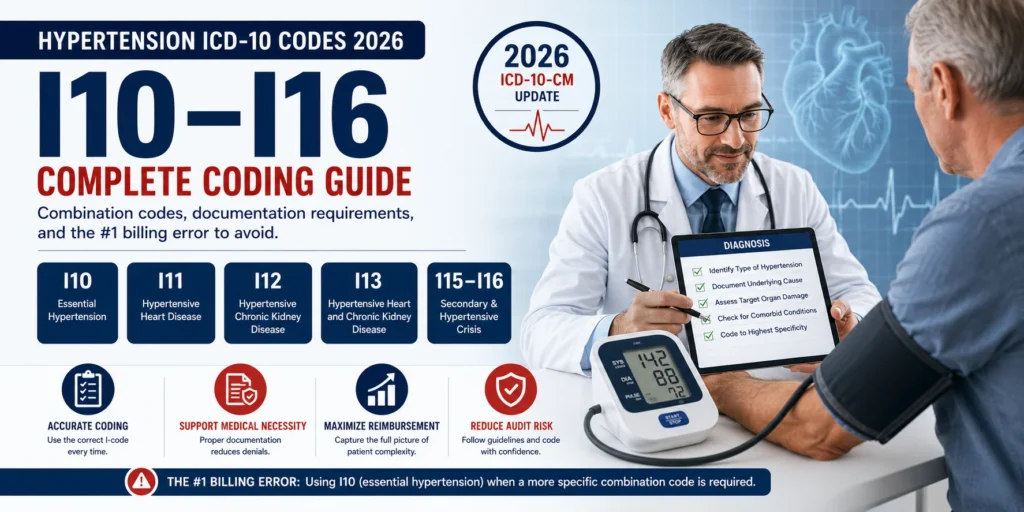

Hypertension ICD-10 Codes 2026 — Complete I10-I16 Billing Guide

Hypertension ICD-10 Codes 2026 — Complete I10 to I16 Billing Guide Nearly half of American adults have hypertension — which makes I10 one of the most frequently reported ICD-10 codes in clinical practice. It is also one of the most frequently coded incorrectly. The single most common error in hypertension billing is using I10 (essential […]

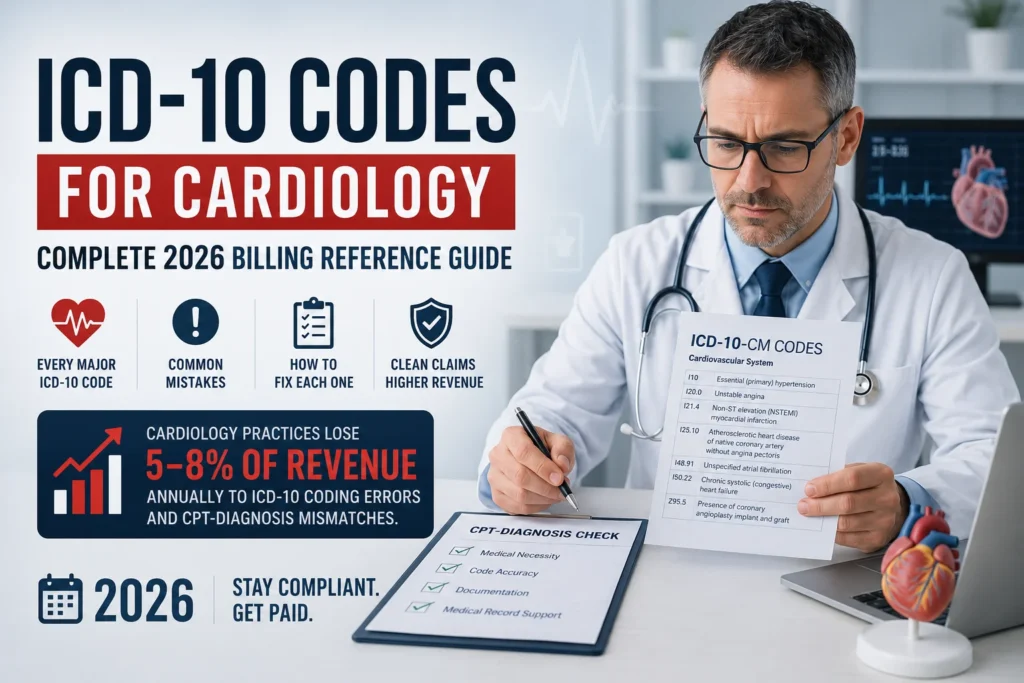

ICD-10 Codes for Cardiology 2026 — Common Mistakes & Complete Reference

ICD-10 Codes for Cardiology 2026 — Common Mistakes to Avoid and Complete Billing Reference Cardiology billing is not like billing for primary care. The stakes are higher, the procedures are more complex, and payer scrutiny is more intense than in almost any other specialty. One wrong ICD-10 code on a cardiac catheterization claim can mean […]

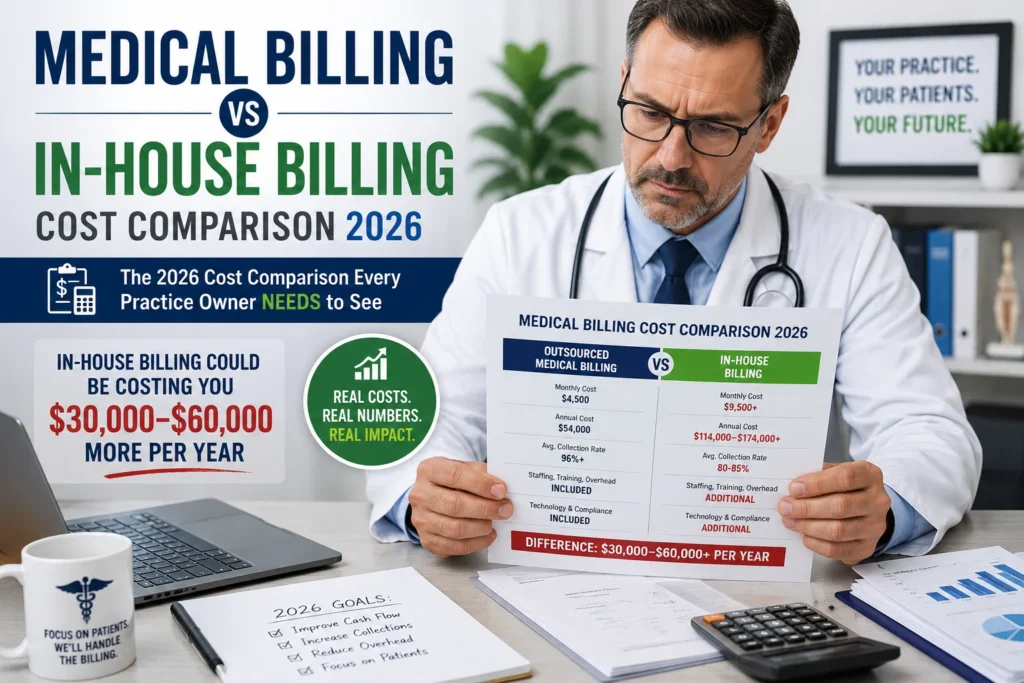

Medical Billing vs In-House Billing | Real Cost Comparison 2026

Medical Billing vs In-House Billing | The Real Cost Comparison for Doctors in 2026 Most doctors make the medical billing vs in-house billing decision the same way. They look at what their biller earns — say, $50,000 per year — add a rough estimate for software, call it $60,000 total, and conclude that outsourcing at […]

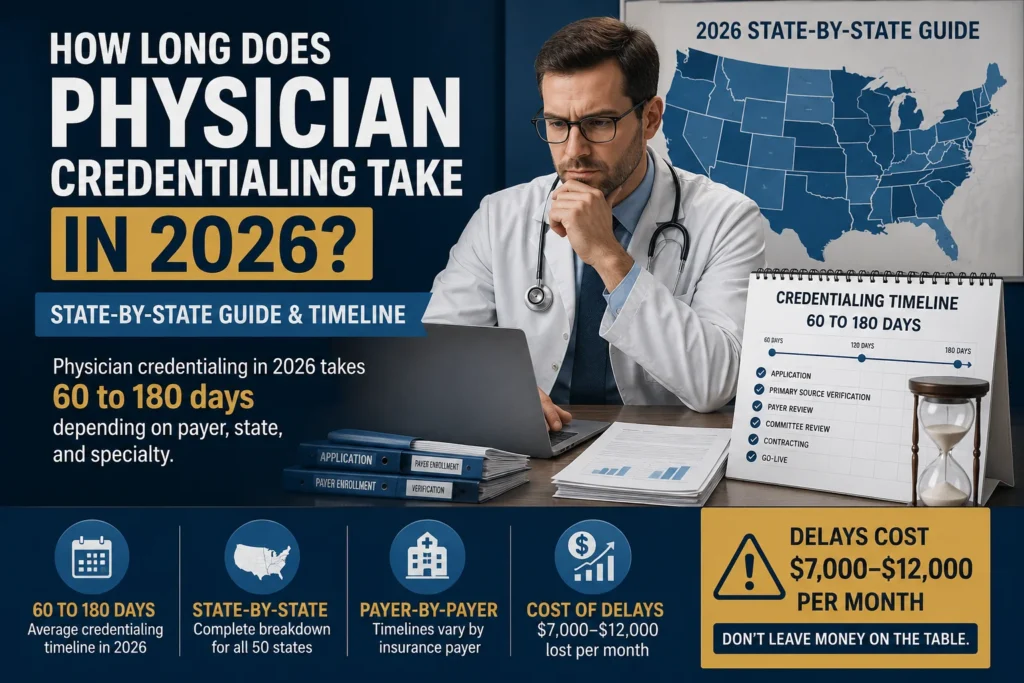

How Long Does Physician Credentialing Take? 2026 State by State Guide

How Long Does Physician Credentialing Take? State by State Guide for 2026 If you are asking how long physician credentialing takes in 2026, you have probably already realized that the standard answer — “90 to 120 days” — is not actually helpful. Because the real answer depends on which state you are in, which payers […]

Top 5 Reasons Medical Claims Get Denied in 2026 | Complete Fix Guide

Top 5 Reasons Medical Claims Get Denied in 2026 — And Exactly How to Fix Each One If that sentence feels familiar, you are not alone — and you are not unlucky. In 2024, initial claim denial rates across the US healthcare system hit 11.8 percent, according to industry data tracked by Experian Health. For […]